The 2025 passage of the One Big Beautiful Bill Act introduced the Trump Account, a unique custodial investment tool designed to jumpstart savings for young Americans. For nearly three decades, families have relied on 529 plans as their primary vehicle for tax-efficient growth for kids; however, the arrival of Trump Accounts, also known as 530A accounts, has shifted the conversation.

What is a Trump Account?

It is a tax-deferred investment account for children under 18, created initially by the U.S. Treasury Department. It functions like a custodial brokerage account until the child is an adult, at which point it converts into a traditional IRA.

The period before the child turns 18 is known as the “growth period.” During this time, special rules apply that differ from standard IRAs:

No Earned Income Required: Unlike a Roth or Traditional IRA, a child does not need a job to receive contributions.

Investment Restrictions: By law, funds must be invested in low-cost index funds or ETFs tracking the U.S. stock market (e.g., S&P 500), with fees capped at 0.10%.

Eligibility & “Free Money”

The prominent feature of this program is the $1,000 federal seed deposit.

As part of the pilot program only U.S. citizens born between January 1, 2025, and December 31, 2028 get the one-time $1,000 contribution. However, any child under 18 with a Social Security number can open an account. They won’t receive the federal seed money, but can still benefit from the account’s tax-deferral and contribution structure.

Trump Accounts vs. 529 Accounts

While both accounts offer tax-advantaged growth for a child’s future, they serve fundamentally different purposes and carry distinct tax consequences.

A 529 plan is specifically optimized for education; contributions grow tax-deferred, and withdrawals are entirely tax-free when used for qualified education expenses. The Trump account functions more like a retirement vehicle, where growth is tax-deferred but ultimately taxed as ordinary income upon withdrawal.

It is important to note that Trump accounts carry a long-term administrative commitment because different contribution sources are taxed differently upon withdrawal.

Here is a side by side comparison of the two accounts:

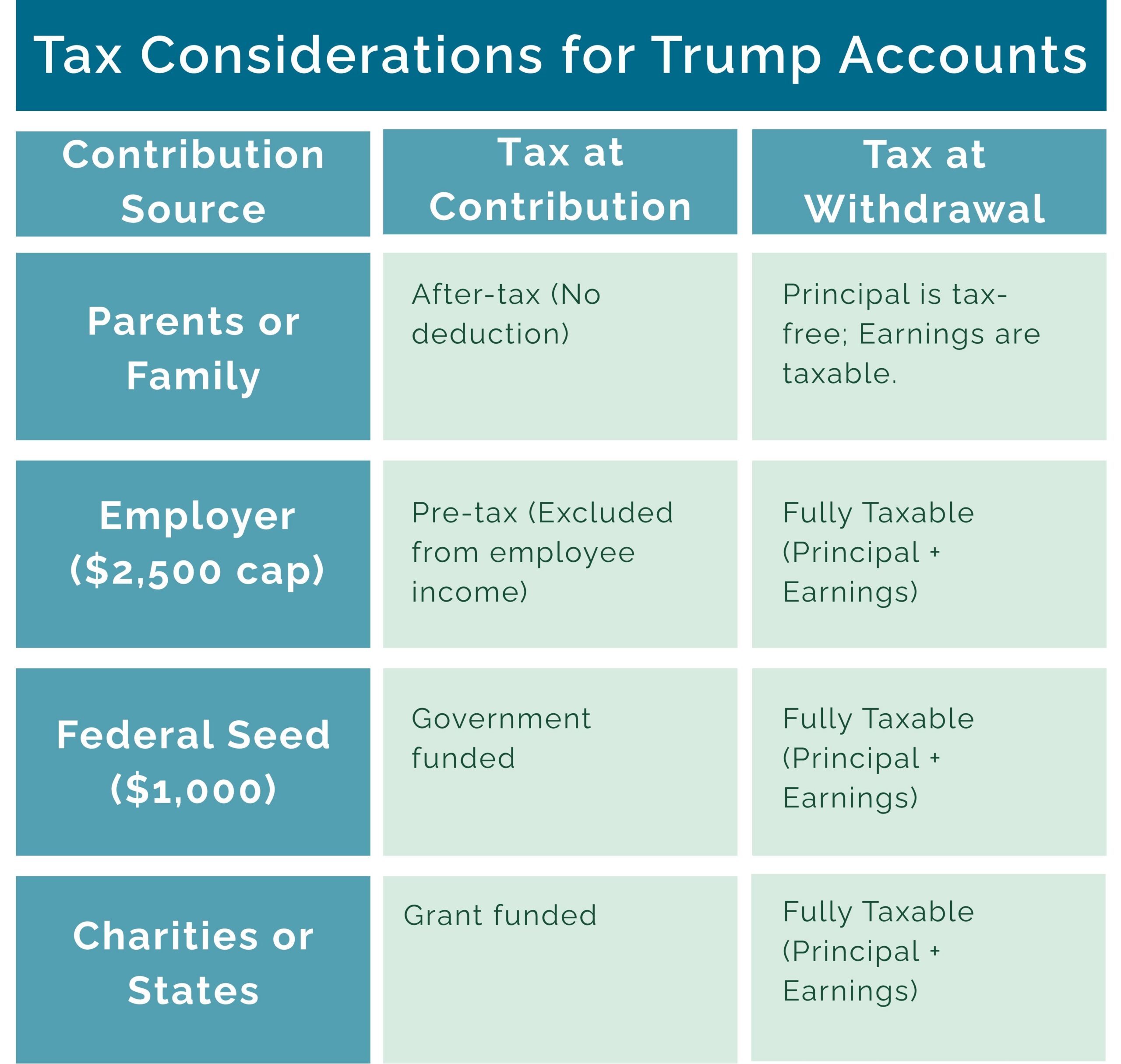

Tax Considerations for Trump Accounts

One important aspect for Trump Accounts taxation is understanding that these accounts hold “mixed” tax attributes. Unlike a Roth IRA where everything is typically tax-free, or a Traditional IRA where everything is taxed, Trump Accounts depend on the source of the funds:

As the Trump Account consists of both pre-tax and after tax money, upon withdrawal the distribution is treated as part return of basis (which is tax-free) and part pre-tax (which is taxable as ordinary income). The tax-free portion is calculated as a pro rata amount based on the proportion of after-tax dollars in the account to the total account size.

The account beneficiaries or anyone who controls the account on their behalf, will be responsible for tracking which dollars are pre-tax and which are after-tax. This will be very similar to using Form 8606, which is used for tracking basis within standard IRAs. Form 8606 will need to be completed with the tax return for all years in which the Trump Account is open.

When does the program officially launch?

The accounts are slated to launch on July 4, 2026, coinciding with America’s 250th anniversary. However, parents can begin signing up now during the 2026 tax season.

The pilot program election can be made on Form 4547 ( to be completed with your tax return) or via the online portal at Trumpaccounts.gov.

After filing, the Treasury Department will contact you with instructions to activate the account.

Alternatively, you can wait until the official launch on July 4th, 2026 to start the process.

Contributions to Trump Account

Starting on July 4, 2026, Trump accounts can be opened and contributed to, on behalf of a child from the year of their birth through the year in which they turn 17. Contributions during this period can be made in three ways:

- Direct contributions

- Employer contributions

- Qualified general contributions

Direct contributions are after-tax, non-deductible cash contributions and can be made by parents, grandparents, friends or the beneficiary themselves. This is similar to a non-deductible IRA contribution.

Employer contributions can be made either to an employee’s own Trump account, or to the Trump account of the employee’s dependent child. Employers’ contributions will be made on a pre-tax basis.

The total amount of combined direct and employer contributions is capped at $5,000 per year in 2026. However, employer contributions are capped at $2,500 per employee. Both these limits will be indexed to inflation starting in 2028.

Qualified general contributions are contributions that can only be made by the Federal government, state or local governments, and 501(c)(3) charitable organizations, which can elect to contribute directly to Trump accounts on their own. For example, as part of the pilot program, children born between January 1, 2025, and December 31, 2028 get a one-time $1,000 contribution from the Federal government. These contributions will also be made on a pre-tax basis.

When can the child use the funds?

The money is “locked” until the child turns 18. Once they reach adulthood, they can use the money for:

- Higher education or job training.

- A first-home down payment (up to $10,000).

- Expenses for starting a small business.

- Retirement (by leaving it in the account as it converts to an IRA).

- The account is a regular IRA account after age 18 and all the regular IRA restrictions apply if the money is withdrawn for purposes other than the ones listed above.

The “Seed Funding” Strategy: A $100,000 Head Start

For children born between 2025 and 2028, the federal government’s $1,000 seed contribution is a wonderful opportunity. While $1,000 may seem modest today, compounding over several years is very powerful. At a target annual return of 8%, that initial seed is projected to nearly quadruple to $3,996.02 by the time the child reaches age 18.

While this won’t cover a four-year degree, it establishes a critical “wealth floor,” ensuring no young adult starts their financial life at zero. The real magic, however, happens at adulthood: by executing a Roth conversion at age 18—when most students are still in a 0% tax bracket – this account can transition into a tax-free vehicle. Without ever adding another penny, that original $1,000 government gift could balloon into over $101,000 by age 60. It is, quite literally, a six-figure retirement foundation built from a single birth-year benefit.

While the new Trump Account offers a powerful head start for the next generation, it is just one piece of a larger puzzle.If you would like to review your specific family situation to see if opening a Trump account aligns with your goals, we are happy to help.